Understanding Credit Bureaus and Their Impact on Your Financial Life

Credit bureaus, also known as credit reporting agencies, collect and analyze credit information on individuals.

- Higher Education

- Article

- Ferrell Business in the News

The three major credit bureaus in the United States are Equifax, Experian, and TransUnion. They operate independently to compile credit reports based on your financial behavior, which lenders use to assess your creditworthiness.

Although credit bureaus do not decide whether you receive credit, they provide the data that lenders use to make these decisions. The information collected includes payment history, outstanding debts, length of credit history, and recent credit inquiries.

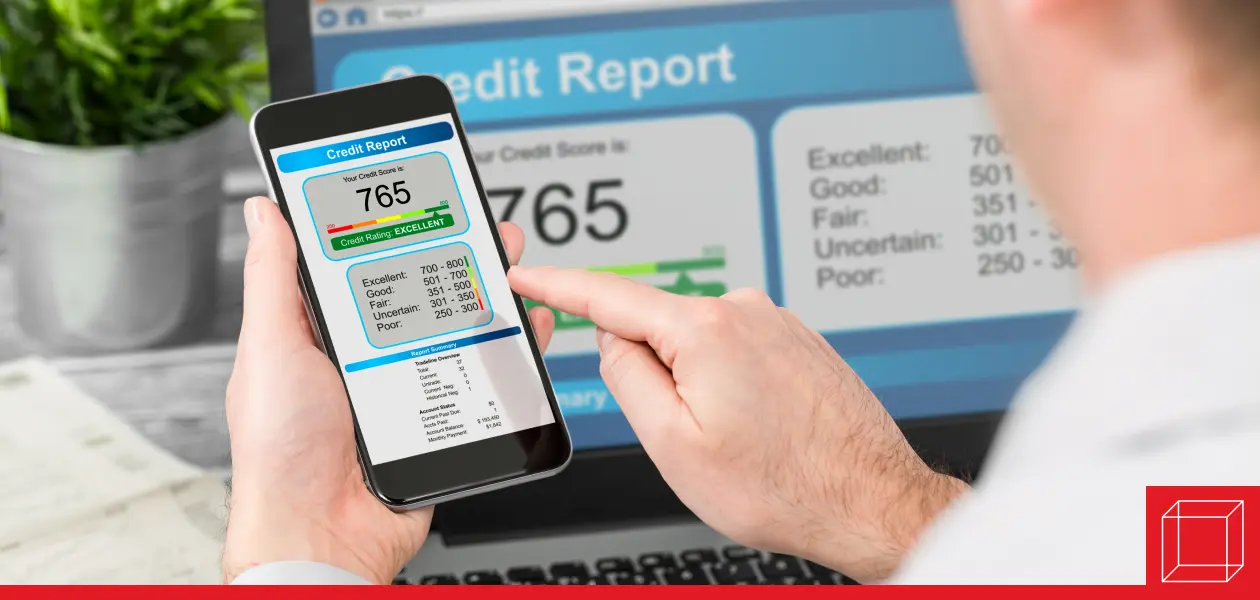

How Credit Scores Are Determined

A credit score is a three-digit number ranging from 300 to 850, summarizing your credit risk. Scores fall into credit score ranges: excellent (720-850), good (690-719), fair (630-689), or poor (300-629). The higher your score, the better.

The two primary credit scoring models are FICO and VantageScore, both of which rely on data from credit bureaus. FICO is the standard used by most lenders.

Factors Influencing Your Credit Score Based on the FICO Model:

- Payment History (35%) – Whether you pay your bills on time.

- Credit Utilization (30%) – How much of your available credit you're using.

- Length of Credit History (15%) – The average age of your credit accounts.

- Credit Mix (10%) – A variety of credit types, such as credit cards and loans.

- Recent Credit Inquiries (10%) – Applications for new credit can temporarily lower your score.

Credit bureaus do not track details like your income, banking history, education, race, religion, political views, or criminal record. Payment history for utilities and rent is usually not included unless you choose to self-report or a provider reports a missed payment.

How Credit Ratings Affect Loans and Interest Rates

Your credit score significantly impacts your ability to qualify for financial products and the interest rates you receive.

Car Loans

- Excellent credit (720+) can secure low or even 0% APR financing.

- Poor credit (below 629) may result in higher interest rates or loan denials.

Credit Cards

- High scores (750+) qualify for premium credit cards with better rewards and lower interest rates.

- Low scores may limit access to secured credit cards or higher-interest credit cards.

Mortgage and Rental Applications

- A good credit score improves your chances of mortgage approval and receiving lower interest rates.

- Landlords may check credit reports before approving rental applications.

Checking and Monitoring Your Credit

Consumers are entitled to one free credit report every 12 months from each of the three major bureaus through AnnualCreditReport.com. Some platforms offer free credit score monitoring.

If your credit score is lower than you’d like, here are key steps to improve it:

- Pay bills on time to build a strong payment history.

- Keep credit utilization below 30% of your total credit limit.

- Avoid opening too many new accounts in a short period.

- Check credit reports for errors and dispute any inaccuracies.

To safeguard against fraud and identity theft, you can freeze your credit with each bureau. This prevents new accounts from being opened in your name without your authorization.

By managing your credit wisely, you can access better financial products and secure lower interest rates, ultimately saving money in the long run.

In the Classroom

This article can be used to discuss the American financial system (Chapter 15: Money and the Financial System).

Discussion Questions

- What are the three major credit bureaus, and what role do they play in the American financial system?

- How do credit bureaus collect and update information about consumers?

- What factors can negatively impact a person’s credit report?

This article was developed with the support of Kelsey Reddick for and under the direction of O.C. Ferrell, Linda Ferrell, and Geoff Hirt

Amanda Barroso and Lauren Schwahn "Credit Score Ranges: What They Mean and How They Work," Nerd Wallet, August 23, 2024, https://www.nerdwallet.com/article/finance/credit-score-ranges-and-how-to-improve

Amanda Garland and Aylea Wilkins, "What Do the 3 Credit Bureaus Do?" Bankrate, January 15, 2025, https://www.bankrate.com/personal-finance/credit/what-are-the-3-credit-bureaus-and-what-do-they-do/

Thomas J. Catalano, "Basics of What a Credit Bureau Is and Does, Plus Major Ones," Investopedia, October 10, 2021, https://www.investopedia.com/terms/c/creditbureau.asp

Geoffrey A. Hirt of DePaul University previously taught at Texas Christian University and Illinois State University, where he was chairman of the Department of Finance and Law. At DePaul, he was chairman of the Finance Department from 1987 to 1997 and held the title of Mesirow Financial Fellow. He developed the MBA program in Hong Kong and served as director of international initiatives for the College of Business, supervising overseas programs in Hong Kong, Prague, and Bahrain, and was awarded the Spirit of St. Vincent DePaul award for his contributions to the university. Dr. Hirt directed the Chartered Financial Analysts (CFA) study program for the Investment Analysts Society of Chicago from 1987 to 2003. He has been a visiting professor at the University of Urbino in Italy, where he still maintains a relationship with the economics department. He received his Ph.D. in finance from the University of Illinois at Champaign-Urbana, his MBA at Miami University of Ohio, and his BA from Ohio Wesleyan University.